Free Trade Agreements (FTAs) help expand foreign markets for U.S. producers and exporters by reducing trade barriers, fostering a more stable and transparent environment for trade and investment, protecting U.S. economic interests, and enhancing the rule of law. To date, the United States has 14 FTAs in force with 20 countries that account for 43 percent of total U.S. agricultural exports to the world. The United States also has concluded negotiations on the Trans-Pacific Partnership (TPP) and is in the process of negotiating the Transatlantic Trade and Investment Partnership (TTIP), which are expected to further enhance U.S. agricultural export opportunities.

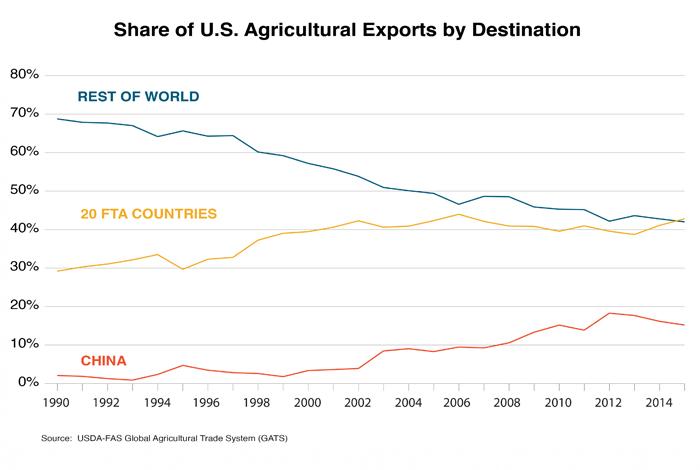

The current 20 U.S. FTA partner countries represent 10 percent of the world’s GDP and 6 percent of global population, yet they account for 43 percent of U.S. agricultural exports to the world, up from 29 percent in 1990, before the majority of U.S. FTAs were implemented. In contrast, the share in U.S. agricultural exports corresponding with the rest of the world (excluding China, which soared as a U.S. market after World Trade Organization (WTO) accession in 2001) dropped from 69 percent to 42 percent.

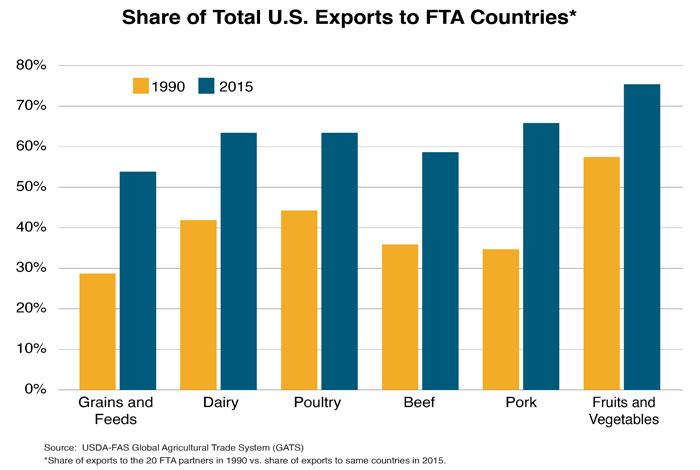

Under FTAs, the majority of U.S. export products enjoy an immediate tariff reduction to zero upon entry into force, with most of the remaining tariffs phased out over time. Immediate improved access is also achieved through duty-free tariff-rate quotas (TRQs) that are sometimes included for sensitive commodities, often leading to full tariff elimination eventually. U.S. exports of the following products to FTA countries had increases of 15 percent or more between 1990 and 2015 as a share of U.S. exports to the world: grains and feeds, dairy products, poultry and products, beef and products, pork and products, and fruits and vegetables. Among these, corn exports to FTA countries had one of the most dramatic growth rates, rising from 22 percent of total U.S. corn exports to 60 percent. A primary reason for the surge was the expansion of TRQs and eventual elimination of all tariff and quota barriers in Mexico to U.S. agricultural exports under the North American Free Trade Agreement (NAFTA). Poultry, beef, and pork exports also increased substantially due to NAFTA, one of the oldest and most comprehensive FTAs the United States has enacted.

NAFTA subsumed the Canada-U.S. FTA, which took effect in 1989, and created a free-trade area involving the United States, Canada, and Mexico. In the 21 years since NAFTA’s implementation in 1994, U.S. agricultural exports to Canada and Mexico have more than quadrupled, growing from $8.9 billion in 1993 to $38.6 billion in 2015. Canada and Mexico’s share of total U.S. agricultural exports to the world has increased from an average of 19 percent (1990-93) to 28 percent (2012-15). Before the agreement, Canada was the fourth leading U.S. market. It is now the number one market for U.S. agricultural exports, and by far the largest U.S. market for high-value consumer-oriented products. Mexico’s imports of feedstuff from the United States are closely linked to its burgeoning poultry and pork industries. It is the top market for U.S. corn, soybean meal, and poultry, as well as the second largest market for U.S. pork.

Analysis by USDA’s Economic Research Service (ERS) found that NAFTA fostered deep integration of North American agricultural markets, characterized by increased cross-border trade of raw material, intermediate inputs and outputs, higher foreign direct investment (FDI), and greater institutional and policy cooperation and coordination (link). Such market integration allows participants to benefit more from their relative strength and spurs more efficient allocation of economic resources. Producers have access to potentially cheaper inputs and FDI, as well as new opportunities to sell their products, though they could face more competition as well.

Increasing intraregional trade also benefits consumers, with access to more competitively priced products, new varieties of food, and off-season supplies of fresh produce. For example, trade liberalization has facilitated U.S. imports of grape tomatoes and fresh avocados from Mexico, while Mexico has become the largest market for U.S. apples and pears. For tropical fruits such as bananas, mangos, pineapples, and others, imports have been filling the demand gaps from a lack of or inadequate U.S. production.

U.S. agricultural exports to Central America and the Dominican Republic more than doubled after the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) went into effect, from $1.9 billion in 2005 to $4.2 billion in 2015. The Dominican Republic is the largest market within CAFTA-DR. At $1.1 billion, U.S. exports to the Dominican Republic constitute 27 percent of total shipments to CAFTA-DR. FAS Santo Domingo reports that CAFTA-DR has established a more transparent process for trade and helped expand imports of high-value products such as red meat, poultry, and cheese, products that had previously faced restrictions. As a result, U.S. exports of consumer-oriented products have more than quadrupled since 2005, led by dairy, beef, pork, poultry products, and prepared food.

U.S. exports to Colombia more than doubled within three years of the beginning of FTA implementation, with rapid growth of corn, soybeans, and soybean meal. The U.S.-Colombia Trade Promotion Agreement also helped catapult the country from the 21st largest U.S. market to the 9th, and U.S. market share in Colombia jumped from 23 percent in 2011 to 50 percent in 2015. Elsewhere, U.S. market share of agricultural imports by Chile and Peru also had remarkable expansions following entry into force of trade agreements. In Chile, U.S. market share grew from 9 percent in 2003 to 15 percent in 2015, led by feeds and fodders, poultry, dairy, beef, pork, and wine and beer. U.S. market share in Peru nearly doubled from 16 percent in 2008 to 30 percent in 2015, with corn, soybean oil and meal, and dairy products expanding the most.

Overall, there is a remarkable contrast between FTA and non-FTA countries in terms of U.S. market share. At 40 percent, aggregate U.S. market share in FTA partner countries is much higher than that in non-FTA countries, which is only 11 percent (or 9 percent, if China is excluded). This dichotomy between the two groups means that on the whole, U.S. exports are much more competitive with FTAs than without.